Levolytics Research #23: Crypto Compression & Expansion Discussion

Available to All Subscribers | All charts free on dudeterminal.com

Welcome to the newest edition of Levolytics Research! The home of actionable data. If you enjoy the research, please subscribe and share our work with friends and colleagues, and follow @levolytics + @permabullnino on X, the Everything App.

Website

Check out Dude Terminal for access to our suite of metrics for:

Crypto

Equities

Macroeconomics

Health

Sports (soon)

Our Take on the Market

In our previous newsletter, we concluded with the following points:

Market-wide panic reigns as investors react to the cloud of uncertainty that comes with AI disruption

The basket of “AI suffering” assets that were sold in November 2025 / February 2026 reaching historically oversold levels across the board

Coinbase trading at a premium vs Binance, which might possibly signal bears are bluffing on this lower timeframe dump

We believed this signaled that downwards impulses in price action were a fake out, which we will follow up on later in the publication

The close of February was choppy and volatile, but not what we’d consider violent per our expectations as of late. Nonetheless we remain steadfast in our expectation that the beginning of March will bring a decisive resolution to the month long $70,000 to $60,000 range for BTC.

Within we will attempt to cover as many bases as possible for readers to better understand how crypto market participants have been reacting to price action, along with the prevalent AI doom / turmoil in the Middle East.

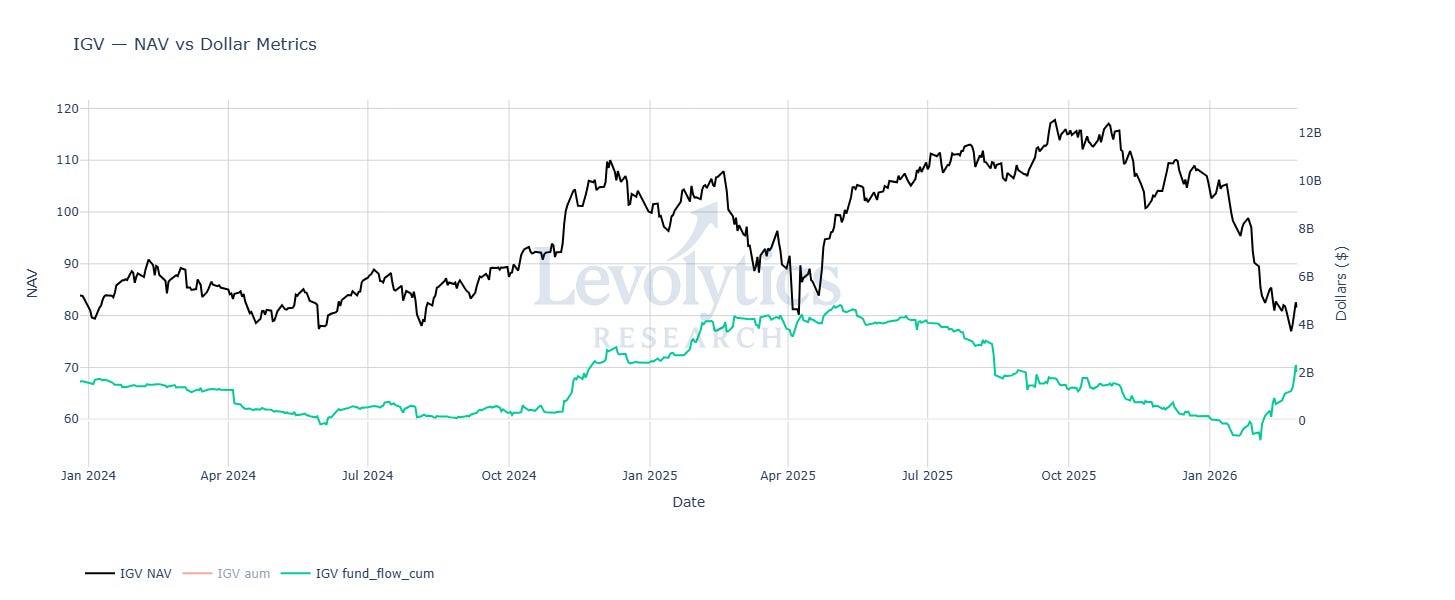

Metric: Net asset value vs cumulative $ flows into IGV since April 2017

Note: 2017 earliest data we could find

IGV = iShares Expanded Tech-Software Sector ETF

This ETF is known as a pure-play software ETF, and has been at the center of discussion as AI fears have overwhelmed market participants

+$3.2 Billion in flows since February 3rd, 2026

Flows ramping up into panic

-2 billion in flows from October 1st, 2025 to February 3rd, 2026

Flows offboarding at the highs

Metric Takeaway:

Data doesn’t lie and always paints the purest picture. Last week we discussed the panic surrounding software - but it’s important to understand when panic is justified. Furthermore, we discussed how crypto was trading as a part of a larger AI doom basket that had been underperforming since Fall 2025.

If you look at the IGV flows above, the bulk of the “panic” seemingly took place at the highs when money was slowly bleeding out the IGV ETF. By the time everyone else was talking about the end of software, flows were already ramping back up.

This is by no means a guaranteed software / crypto bottom, but following the data / money does provide better odds for strong outcomes:

22-day % returns for IGV stocks at bottom 10% oversold levels (see Levolytics #22)

Duration of drawdown is currently 40 days i.e. 40 straight days of negative 22-day returns

Bottom 10% performing periods begin at 18 continuous days of negative returns

NOW we have signs that flows are ramping up into this drawdown

Software is one example of the AI doom basket reaching oversold levels. Let’s jump into crypto to see how it compares.

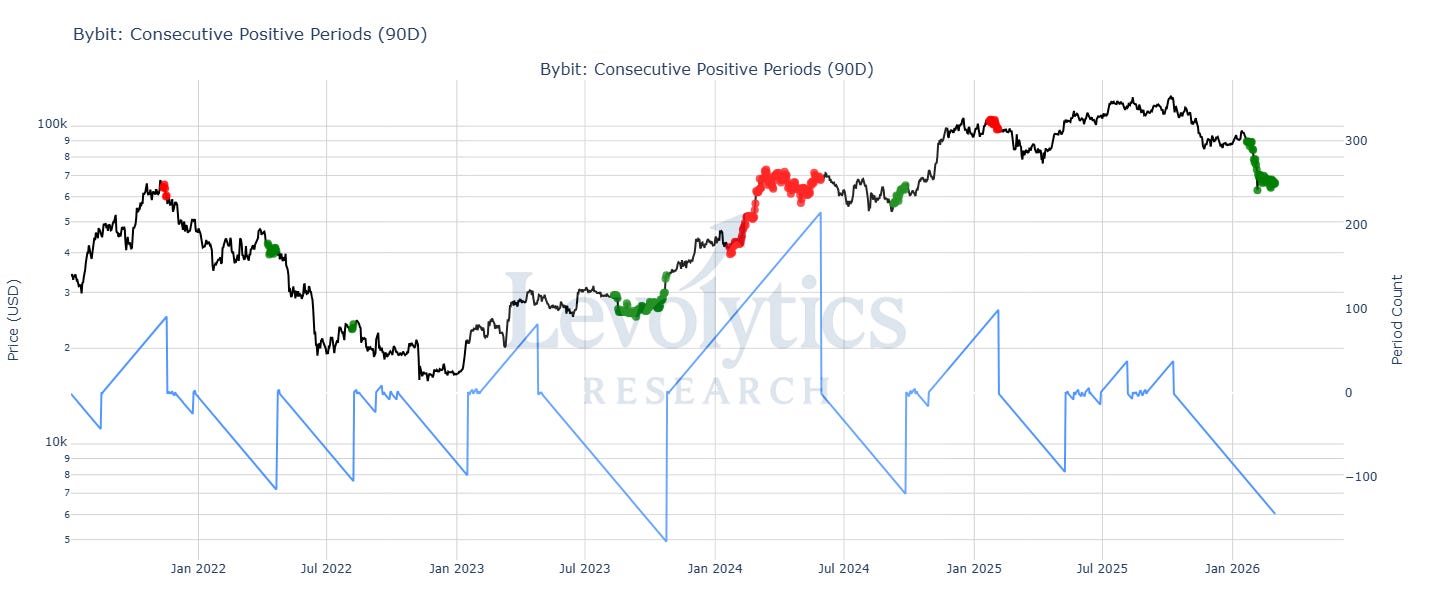

Metric: Consecutive periods (1D candles) of positive or negative 3-Month % returns vs USD across all altcoin perp pairs on Bybit

Current value = 144 consecutive days of negative 3-month % returns

Bottom 10% values begin at 99 consecutive days or more

Metric Takeaway:

The easiest way to tee up the state of crypto is with the gentle reminder that we are within a larger, extremely overextended downtrend.

Keep in mind there are normal downtrends with dead cat bounces along the way. This is not the case over the past ~5 months - it has been down only, with little relief.

Every time we get price compression / consolidation, it’s time to pay attention. Why? Because there’s an ever growing potential of a very strong relief rally. Does that mean a “bear market bottom” or “up only”? No. But mean reversion on a large scale is festering and building under the hood of this market. Time tells this story best.

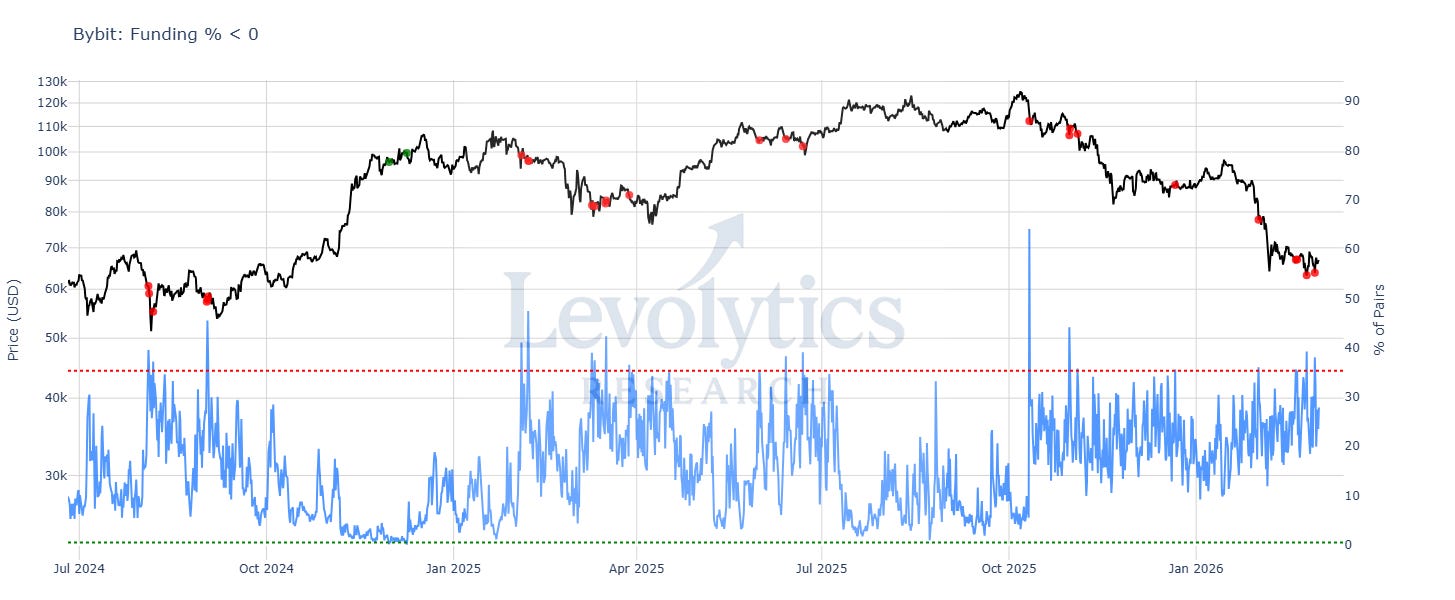

Metric: % of perpetual swap pairs on Bybit w/ funding rate < 0

Past few weeks values have been hitting historically high levels around 35%

Metric Takeaway:

Funding rates go negative as a function of 1 of 3 things:

Perp traders shorting or

Long liquidations (forced selling) or

Spot traders buying

Price has been sideways for a month, so we are attributing this to a combination of (1) complacent bears shorting after an endless downtrend and (2) spot buyers stepping in.

One other thing worth paying attention to here is the persistence of these high value prints, which can be seen in the red dots on the price chart above. We also believe this adds to the theory that what we are seeing right now is persistent shorting from futures traders or persistent buying from spot traders.

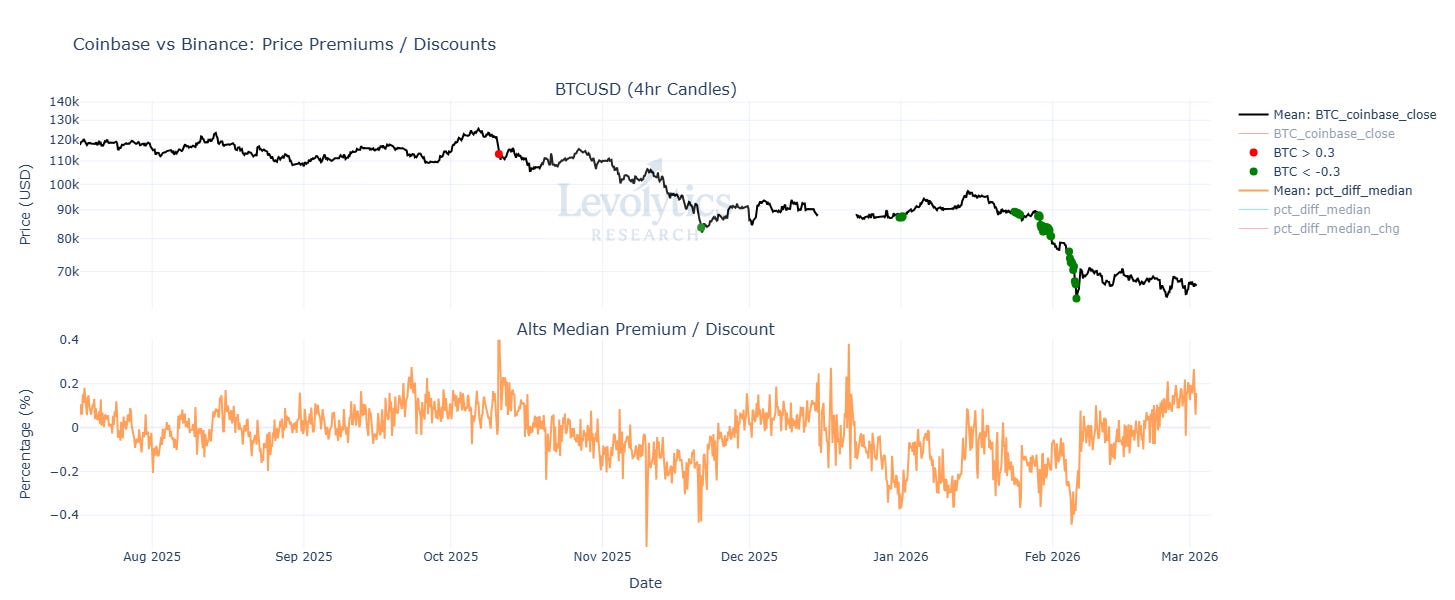

Metric: Median Coinbase vs Binance Premium / Discount for all altcoins on both exchanges

Positive values = Coinbase premium

Current value = 0.157% Coinbase premium for altcoins

In late December 2025 and January 2026 the discount widened and was persistent

Coinbase premium has been increasing for almost a month now

Currently 46% of pairs trading at a premium, largest value since mid December 2025

Metric Takeaway:

Last week we said the following, which we believe is extremely important in the current market environment:

We particularly like looking at this metric because in theory it feels difficult to cheat - altcoins are the risk assets of crypto so there should be an urgency to sell them if BTC is expected to make another leg lower. That urgency to sell isn’t currently revealing itself in the Coinbase premium / discount.

Both large legs down in the past 5 months had consistent Coinbase discounts leading into them. Until we start seeing a discount again we believe there’s reason for optimism.

This metric also supports the funding rate chart in that there’s definitely a spot bid contributing to negative funding rates we are seeing.

Metric: 30 & 90-Day % change in Total Stablecoin Market Cap

Current values:

30-Day % Change = 0.87%

90-Day % Change = 1%

Last period 30 and 90 day % change flipped was in June 2022

Likely result of the Terra LUNA collapse

Metric Takeaway:

Flows play a large role in the contraction / expansion of the broader crypto asset class. After 90-day stablecoin flows flipped negative in 2022, it took almost 18 months before it flipped back to positive. In our opinion, this will not be the case this time around. These are our thoughts instead:

As of this moment, stablecoin flows have stalled - not gone though a sustained, significant contraction. Relative to the past few years, yes, growth is slow. However - in the grand scheme of things, this isn’t the giant exodus out of crypto that some people have been talking about. Just a lack of new money.

Blockchains do a handful of things very well, and one of those is dollarizing the planet. This is also no longer a secret - and ~$300 Billion in stablecoins isn’t the final destination. Trend of up only likely continues.

The fact that this trend is likely up only (in our opinion) shows the significance of this extended period of consolidation. We believe there is a non-zero chance this will be looked back on as a sign of capitulation.

An ever growing pocket of crypto is going into yield bearing stablecoins. Rates are cyclical and follow price - which is likely impacting the expansion of this sector as well.

Simply put - sideways isn’t great. But these data prints are not worthy of panic yet in our opinion.

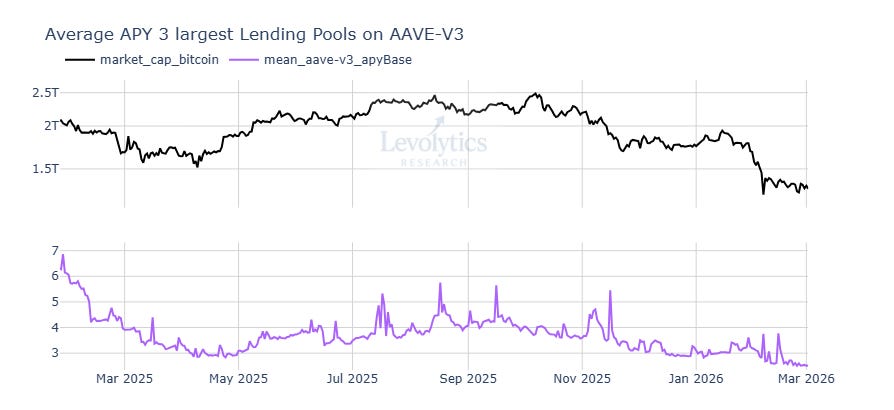

Metric: Average APY for top 3 largest lending pools on AAVE-V3

Current value = 2.5%

Lowest value since V3 launch

Total value currently loaned in these top 3 pools = ~$12 billion

Metric Takeaway:

Yields are at rock bottom levels. This matters, and plays a large role in crypto market expansion cycles. A quick simplification of this cycle is listed below:

Prices go up

Traders borrow to get more long

Yields increase

Stablecoin inflows increase to capitalize on yields

Note that the initial driver here is PRICES UP. We are in the middle of one of the longest persistent downtrends in a long time in crypto. There’s been zero opportunity for yields to spike. Now here’s the crypto contraction cycle:

Prices down

Traders deleverage

Yields decrease

Stablecoin outflows increase as there’s no money to be made in crypto

Prices going up solves a lot of problems. And most importantly - we believe that they remain the key driver for yields and stablecoin inflows going up. That could change in the future, but for now they remain in the driver’s seat.

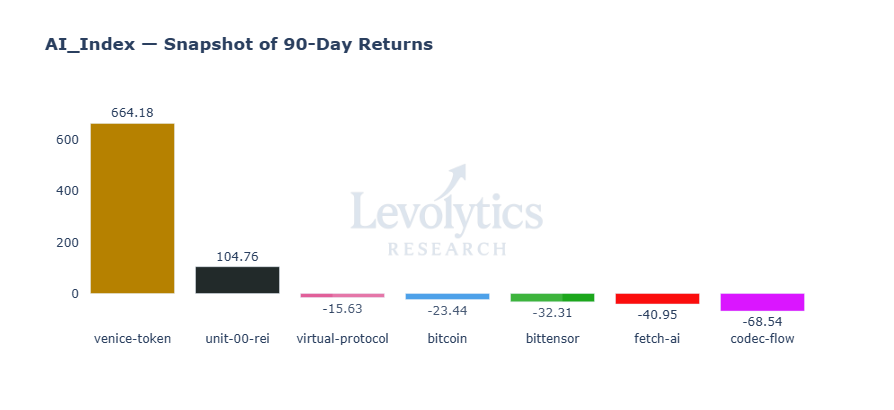

Metric: Snapshot of 90-Day % returns for relevant AI coins

Metric Takeaway:

We expect this sector to bottom the fastest when the time comes, or when we look back on the bottom in the rearview mirror. AI is all the rage, and access to it in equity markets is expensive relative to crypto. Pay attention to AI price action as a gauge for the market’s early risk appetite.

Our Approach

Takeaway

The analysis above highlighted the following:

Doom basket of software + crypto both very oversold

Software historically large drawdown + inflows at range lows + high volume traded

Crypto historically long downtrend

Duration of crypto downtrend has caused:

Deep compression of yields within crypto ecosystem

This has probably impacted stablecoin inflows

There’s been NO money to be made in crypto

Funding rates persistently negative

Indicative of comfort in getting short + persistent spot bid

Coinbase premium showing there’s a spot bid

AI sector in crypto is important to watch moving forward, likely faster mover

Crypto remains an extremely reflexive asset class, and we strongly believe that the endless down-only price action has sucked all the air out of the room.

We also stubbornly hold the belief that this market is extremely oversold and that a relief rally if / when it happens will be quick and violent.

It’s also important to remember when reading our research that our bullishness should be measured by our % exposure in the Levolytics portfolio. More on this to follow in the sections below.

Macro Approach

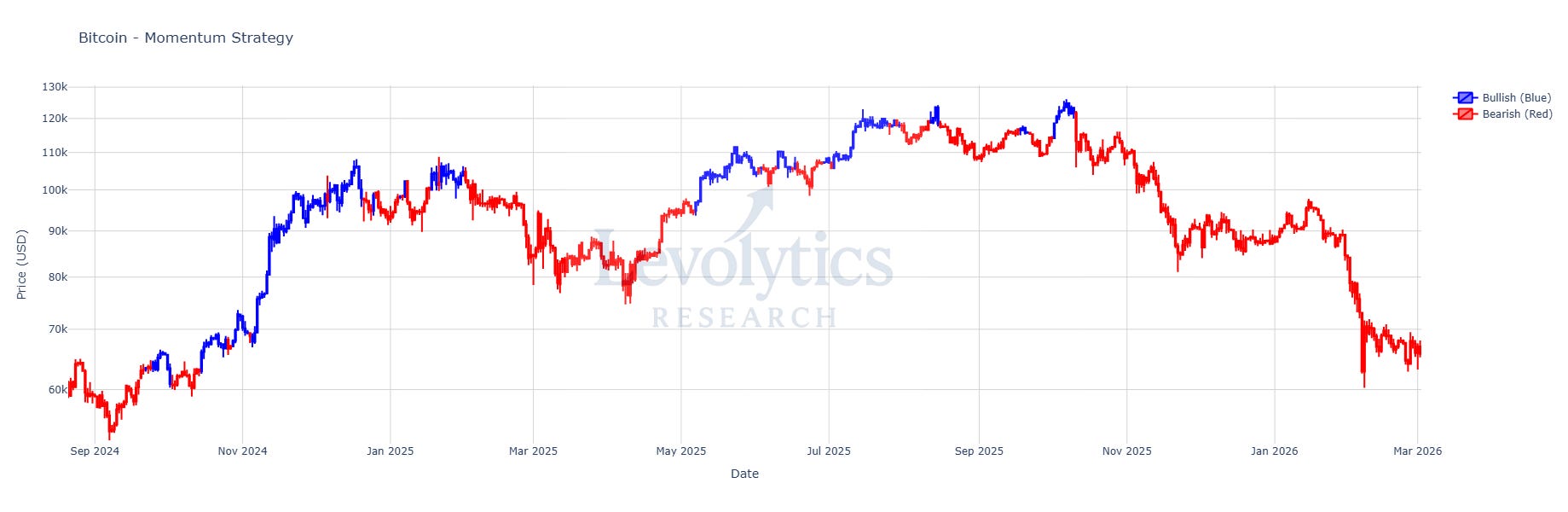

Our macro momentum indicator is still printing bear for BTCUSD. As we’ve mentioned before - until BTC gets moving upwards we’re keeping our portfolio exposure capped.

We want to see BTCUSD hold above the blue box here. Something has to give, and soon. Our target is still the $76,000 - $80,000 area if an upside breakout is granted.

Strategy

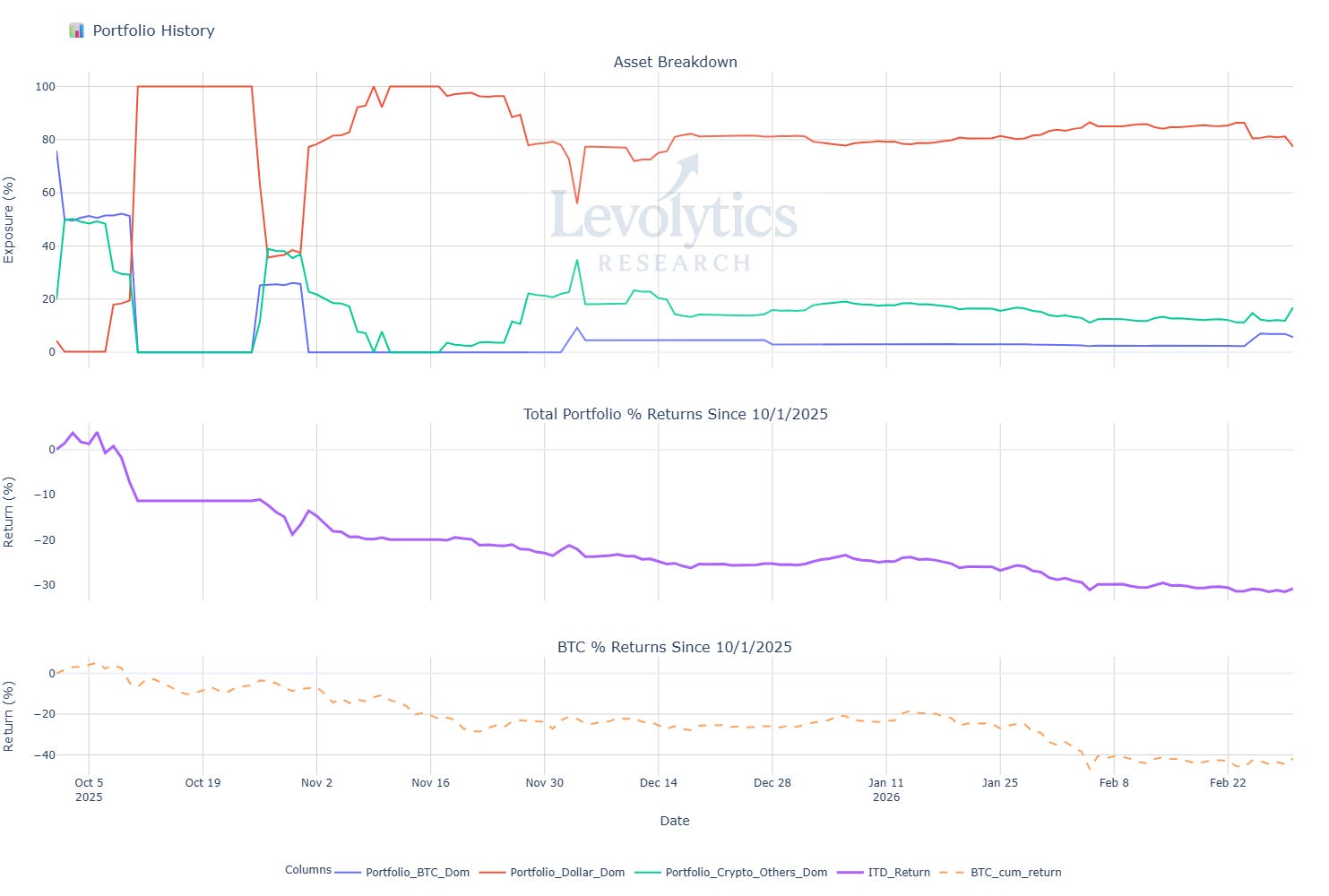

Our current portfolio composition is as follows:

% of Portfolio in BTC = Blue line

Current value: 5.70%

% of Portfolio in Crypto Alts = Green Line

Current Value: 16.92%

% of Portfolio in Cash = Orange line

Current value: 77.39%

Inception to Date Returns = Purple line

Current value: -30.81%

BTC Returns Since Inception = Dotted Orange Line

Current value: -41.79%

Note: Levolytics Research liquid strategy went live October 1, 2025.

Explanation:

We’ve tacked on a bit of exposure into a few of our favorite fundamental plays that are starting to show strength on lower timeframes. Some of this has been applied via reshuffling funds from other assets and the other chunk with small cash injections.

We’re still moving slow waiting for our ideal conditions to materialize. When they do we will deploy with conviction.

Sign Off

We still believe crypto markets are overdue a rebound, but it remains to be seen if it’s a “dead cat bounce” within a prevailing bear trend or a proper macro bottom before a new bull run.

Patience is still warranted - do not forget crypto is an extremely reflexive asset class so bucking the bear off our backs is going to be difficult.

AI sector will likely be the fastest moving area for price action within crypto - it will likely bottom and top first for the foreseeable future.

Stay patient and vigilant,

Disclaimer

The performance results presented herein reflect proprietary trading activity conducted with internal capital only. No external capital is managed, accepted, or solicited. These results are unaudited and are provided solely for informational and research purposes.

Performance data represents the return on internal capital based on realized and unrealized gains and losses, net of trading fees and transaction costs, but before any taxes or potential operating expenses. The methodology used to calculate performance has been applied consistently; however, results have not been verified by any independent party.

Past performance is not necessarily indicative of future results. All investments involve risk, including the potential loss of principal. The information contained herein does not constitute an offer to sell or a solicitation of an offer to buy any security, investment fund interest, or other financial instrument.

Any opinions, estimates, or forward-looking statements are subject to change without notice and are provided for illustrative or educational purposes only.